THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES FOR MORE INFORMATION

It’s the new year and you are ready to make some changes to your finances.

It’s the new year and you are ready to make some changes to your finances.

Since you’ve got your best friend motivation on your side, let’s take some time to look at some simple ideas to give your finances a fresh start.

I’m not talking big changes that are going to take a lot of effort.

Instead I am talking about little things that you can do to improve your financial situation.

By doing these little things, you will help keep your motivation high, which will result in you tackling more and more items, helping you to improve your finances every day.

And by improving your finances little by little, you will see massive change. Not overnight but in time.

In fact, if you make it a point to complete many of the ideas on this list this year, come December you will see your money situation is drastically different.

All because you did a bunch of little things throughout the year.

So let’s get started on looking at the ways to give your finances a fresh start this year!

Table of Contents

50 Ideas For A Fresh Financial Start

#1. Clean Out Your House

Over the years, we accumulate a lot of stuff. Some of this stuff we use, but most if it gets packed away and is never used again.

So take a weekend and clean out your house.

Go room by room and see what you no longer use or need.

Then put them onto one of 3 piles:

- Garbage

- Donate

- Sell

The first two piles are clear what to do.

If the item is worthless to you and isn’t valuable to anyone one else, toss it in the trash or recycle it if possible.

If there is some value to the item but not to you, donating it to someone in need is a great option.

For the sell pile, you need to take your analysis one step further.

If the item is valuable, can you sell it and make some money for yourself? If not, then most of these items can be donated as well.

But if you can make some money selling the items, here is your plan of attack.

Take things like old cell phones, video games, DVDs, etc. and sell them on Decluttr. They tend to give the highest payout on these items.

Just enter in the items barcode to see how much Decluttr will pay you.

If you feel this is a fair price, add the item to your list and Decluttr will give you a packing label so you can ship your things for free.

When Decluttr receives your items, you get cash.

For everything else, look at Facebook Marketplace or Craigslist to sell the items.

Be sure to offer the items for a reasonable price.

The goal isn’t to become a millionaire by selling your unwanted things.

The goal is to clean out your house and to make you aware of how you spend money on things you really don’t need or want.

Of course, making some money in the process is also a benefit.

#2. Increase Your 401k Contribution

This one is so simple, it will take you 5 minutes to complete. You don’t need to increase your savings rate by a lot here, just by 1%.

If you are making $40,000 this comes to $15 per paycheck. You can afford to do this.

And before you tell me that an extra $15 isn’t going to make a big difference, think again.

An extra $15 each time you are paid that grows at 8% for 20 years comes to nearly $20,000.

Wouldn’t it be nice to have $20,000 more just by taking 5 minutes to check a box?

If you have online access to your 401k plan, you can update your contribution amount yourself.

Otherwise, reach out to your human resources department and ask them for help.

#3. Open An IRA

If you aren’t covered by a 401k plan at work, here is how you save for retirement.

Open a Roth IRA at Betterment.

The process will take you all of 10 minutes and Betterment will handle all of the investing of money and rebalancing of your account.

You can forget about the account and let time and compound interest work its magic.

When you set up your account, try to save as much as you can each month. Aim for $100 if you can swing it.

But don’t get discouraged if you can only afford to invest $20 a month right now.

Regardless of the amount you can afford to invest, take the time to set up a meeting in your calendar for 6 months or 1 year from now.

Title it “Increase my Betterment savings rate”. When the day comes and you get the notification, log into your account and increase your monthly transfer amount.

Finally, if you are covered by a 401k plan at work, I still encourage you to open a Roth IRA account with Betterment.

I go into detail why the importance for both types of accounts in this post.

#4. Automate Your Savings

And while we are on the subject of saving more money, set up an automatic transfer to save money in a savings account too.

It doesn’t matter how much you save, just make it a habit of saving money. Too many of us plan to save at the end of the month but never do.

So set up an automatic transfer every time you get paid. Your employer might even allow you to split your paycheck if you have direct deposit.

As for the savings account, don’t use a traditional bank. They don’t pay any interest.

Use an online bank where you can earn interest and have your money grow faster.

My favorite is CIT Bank. They tend to pay the most interest and make saving money simple.

#5. Do Your Taxes ASAP

Most people get a nice refund every year when completing their taxes.

In fact, the average refund is close to $2,000. The longer you wait to file your taxes, the longer it is until you get your money back.

In addition to this, the longer you wait to file your taxes, the greater the risk you run of becoming a victim of identity theft.

Every year more and more taxpayers are victims of this crime.

Don’t risk your refund and the headaches that come along with having your identity stolen and file your taxes as soon as possible.

#6. Reevaluate Your Tax Withholding

Speaking of a big refund, it is awesome to open the mail and see a check worth $2,000 versus a credit card bill.

But by getting that large refund check, you are doing yourself a disservice. You can simply change your tax withholdings and get a larger paycheck all year long.

And if you are smart enough to follow through with the earlier tip and open an account with CIT Bank, you will have more money than that refund check!

Here is how this works.

Let’s say you do nothing and get a $2,000 refund check.

By the time the check comes, you have already thought of all the ways you are going to spend the money.

A new smartphone. A nice vacation. Maybe even a few dinners out.

Before you know it, the money is gone and you are in the same financial position you were before.

But let’s say you adjust your withholdings and your biweekly paycheck is $75 more because of it.

You take the $75 from each paycheck and put the money in your CIT Bank savings account.

When it comes time to file your taxes, you find you are getting a refund of $500.

Seeing this small amount might disappoint you.

But you saved $1,950 in your savings account for the year. And with interest it currently sits at a little more than $2,000.

By adjusting your withholding and saving the money, you have more money than if you got a big fat tax refund.

If the above doesn’t convince you that you need to adjust your withholdings because you just love that huge refund check, here is another option.

When you get your refund check, don’t spend it all that night. And don’t have a plan for the money before you even get it.

When the check comes, break it up like this:

- If you have credit card debt, student loans or an auto loan, use 50% of the refund towards the debt.

- Then take 25% and put it into a savings account.

- Take the remaining 25% and spend it however you want.

If you don’t have debt, then save 75% of your refund and spend the other 25% as you please.

If you do this, you still have money to spend as you see fit but you are getting ahead financially by paying down debt or building up your savings.

#7. Try Budgeting For A Month

Do you know where you money is going or where you spend the most money each month? If you don’t then you need to set up a budget.

I know what you are thinking.

You don’t have the time. A budget is too much work. Insert any other excuse you can think of here.

You are wrong.

There are some simple options out there that make budgeting easy and dare I say, enjoyable?

My favorite budget is Tiller, mainly because I enjoy working with spreadsheets. Tiller automates the most time consuming part of a budget so all you have to do is confirm the expense category.

It literally takes 5 minutes a day.

If the idea of a spreadsheet budget interests you, you can check out this great list of free budget templates you can download.

If spreadsheets aren’t your thing, you can use an app.

I like GoodBudget. The free version should be enough for most people, though there is a paid version as well.

At the very least, write down every penny you spend for one month, then look it over. I bet you will be surprised to see some of the numbers.

#8. Review Your Budget

If you followed my tip above to start a budget or you have been following a budget, you need to take things one step further and actually review it.

After all, what good is a budget if you never look at it?

You could be overspending and not realize it.

The point is, life changes and so does your spending. If you set up a budget but don’t review it, you have no idea if you are getting ahead financially or not.

So take 30 minutes once or twice a month and look over your budget to make sure it still reflects your spending and is helping you to reach your financial goals.

And here is a bonus trick if your life is super busy.

Use Personal Capital to budget.

I set up the categories in my budget that I tend to overspend in, like groceries and eating out. These categories then show right on my dashboard in the app.

All I do is log in and my budget is updated to the minute. So I see where I stand every time I log in.

Click here to get started with Personal Capital!

#9. Give Cash A Try

When was the last time you relied on cash for your spending?

If you are like most people, you pay with cash from time to time, but most of your purchases are with debit or credit cards.

Take a week and live on cash only. You will be stunned at what you realize.

When I tried this for a week, my spending decreased to close to nothing. Give it a try and see for yourself how powerful it is.

#10. Eat At Home

I admit I love to eat out.

The variety of food choices and the atmosphere pulls me in each time. But eating out too often can destroy your finances fast.

I’ve since cut back a little bit and my finances have improved dramatically.

It’s no surprise that when you buy food at the grocery store you get more for your money.

I still dine out, but not as frequently. And when I do go out to eat, I’ve learned some tricks to help me slash my spending too.

By using this plan of attack, I still get to indulge by eating out and I save money at the same time.

#11. Plan Your Meals

Of course, a key part of getting more for your money at the grocery store is to meal plan.

This simple strategy will not only allow you to buy the most for the lowest prices, but will yield you leftovers too.

It’s a win-win.

And odds are you will be eating healthier too, which only helps your waistline and your future finances.

#12. Cancel Memberships

Do you know how much money you are wasting?

Probably not.

With so many things these days set up as a monthly subscription, it is easy to lose track of where your money is going.

Take the time to review your memberships and subscriptions and see which ones you don’t use or no longer make sense for your lifestyle and cancel them.

There is no reason to pay for something you don’t need or use.

And if you don’t have the time to do this yourself, use Trim. This service will review your spending and offer suggestions for where to cut back.

It will even negotiate your cable bill too! On average they lower cable bills by $30 a month! And they do it all for you!

#13. Set A Savings Goal

As important as it is to pay yourself first, it helps if you have a savings goal. Take a few minutes to see what you want but cannot afford.

This can be anything from a house, to Christmas gifts, or even building an emergency fund.

Once you have your list, figure out how to save money to reach your goal.

This is a lot easier than it sounds.

Ideally, you will save something every month towards your goals.

For example, to save $1,000 for Christmas gifts, divide $1,000 by the number of months until you need the money to see what you need to save each month.

If it is March, divide $1,000 by 10 and you will need to save $100 a month.

Just be sure to put the money into a savings account so you know you will have it.

I recommend CIT Bank. Opening your account is simple and they offer one of the highest interest rates, meaning your savings will grow faster.

Click here to open your account today!

When you have a goal tied to your savings, you are more likely to stick with it long term and see results.

#14. Limit Guilty Pleasures

What are your guilty pleasures? Take a couple minutes to write them all down.

Don’t be embarrassed, no one is judging you here.

Now look them over and see which ones you can scale back on.

For example, if your guilty pleasure is eating a giant bowl of ice cream after dinner, can you cut back to only eating it every other day?

Or maybe eating a smaller bowl?

Whatever change you can make to cut back will help you and your finances.

And if your guilty pleasure is bad for you, like smoking, try your best to cut this out completely.

It isn’t easy, but you will be much better off in the long run.

#15. Review Your Transportation

Do you own multiple cars? Do you live in an area that has great public transportation?

Take some time and consider getting rid of your vehicle.

Owning a car costs a good amount of money when you take into consideration gas, maintenance and insurance.

If you got rid of your car, you could save money.

This one might be a stretch for some, but try to keep this is mind.

When we make ourselves feel uncomfortable and stretch, we grow and become a better person.

So instead of just completely dismissing this one, take a couple minutes and think about it.

You don’t have to take action, just consider it for a minute.

We did this last year. We thought of the advantages and drawbacks of switching to a one car family.

In the end, we decided that we still do need two cars, but were surprised at the many strong reasons to get rid of one.

And one day, we very well may.

#16.Comparison Shop

Doing this trick takes a little bit of time but pays for itself quickly.

The next time you want to buy something, don’t just visit one store or website and buy it.

Take the time to do a little research to see if somewhere else offers it for less or even has a coupon.

Thanks to the internet, retailers have to offer great prices to survive. So chances are you can find comparable prices at other retailers too.

When I did this recently, I saved close to $70!

Another site had the item on sale and offered a coupon that I could apply on top of the sale price.

And don’t overlook cash back websites too.

By shopping through a cash back website, you not only get to use coupons to save money, but you earn cash back as well.

My two favorites are Ebates and Swagbucks.

I simply visit each one before I buy anything online to see how much cash back I can earn since they can vary.

Recently I saved over $150 doing this. I used a coupon to get a discount, then earned 5% cash back from Swagbucks, and since I used my cash back credit card, I earned another 2% cash back.

Just remember to sign up for both to maximize your savings!

#17. Save Your Spare Change

Ever since I was a little kid, I’ve always collected my spare change in a jar.

Back in the day, I would go through this jar and puts my coins into rolls and take them to the bank.

Nowadays most banks won’t accept rolled coins so you are stuck with finding a bank with free coin counting.

First try at the bank you have accounts with, then go from there.

If you are forced to use a Coinstar machine, stick with a gift card instead of getting cash back. The fee they charge for cash is crazy high.

When I cash in my spare change at my bank, I regularly end up with around $200 that I then invest.

#18. Save Money On Water

Water bills aren’t typically too high, so most of us ignore some simple tricks to reduce our water usage.

Even though your water bill might not be high, taking simple steps can reduce this bill and allow you to save more money.

Here are some simple ideas:

- Turn off water when brushing your teeth or shaving

- If you wash dishes by hand, don’t let the water run the entire time

- Install low flow shower heads and faucets

- Reduce loads of laundry by combining into bigger loads

Lastly, you can opt for a low flow toilet.

But if your current toilet is in good condition, then don’t spend the money to replace it. Instead put a brick or a plastic bottle filled with water in the tank.

This will effectively help you to use less water on every flush.

#19. Save Money On Cleaning Products

Have you noticed how expensive cleaning products have become?

Having to stock up on different cleaners can easily break your budget.

Luckily there are some simple things you can do to save some money.

You could buy generic brands to save money. Or you could make your own.

By using simple ingredients that are also environmentally friendly, you can save money.

#20. Buy Generic Brands

Speaking of buying generic, take this one step further and start buying store brand groceries as well.

Trust me when I say you won’t be able to tell the difference. I started eating store brand food when I bought my first house and money was extremely tight.

At first I was nervous to do this, thinking the taste would be off.

But it wasn’t. In fact, I couldn’t tell the difference on most of the foods I bought.

The best part is store brands cost a fraction of the cost that name brand foods do. The end result will be a fatter wallet for you.

#21. Make Shopping Lists

Do you ever look at how much you spend on groceries and other things and wonder if there is a simple way to save money?

There is and it is called making a list.

When you make a list before you go shopping you save money in two ways.

#1. You don’t get sucked into impulse buys. Advertisers are good at getting you to buy things. By sticking to your list, you can avoid this temptation.

#2. You only buy what you need. When you have a list, you know what you need. You never have to stop and wonder if you are close to running out of mustard, buy it and then see you have 4 unopened containers in the pantry.

The only catch is you have to follow your list. You can buy everything on your list and nothing more.

#22. Shop With A Smaller Cart

This is a great trick most people overlook.

When you are shopping, pick the smaller shopping cart over the large shopping cart.

Or pick a shopping basket over a cart.

By using a smaller cart or basket, you have less room for stuff. As it fills up, you will begin to question your purchases and might even skip buying something for this reason.

Many times we put things on our shopping list that we do need, but don’t need right at this moment.

By choosing a smaller cart, you trim your list down even further, saving money.

#23. Clip Coupons And Other Discounts

It doesn’t take long to scan through the coupon inserts to see if there are any discounts you can use on the products you buy.

But you have to be careful.

Too many of us see a coupon for a product we don’t buy but clip the coupon and buy the item because we think it’s a great deal.

This is great if you are open to trying different brands of products you use, but not if you are just buying things because there are coupons.

Alternatively, you can follow companies on social media to get access to special coupons and discounts.

You might even consider joining their mailing list.

Just be prepared to get a lot of emails.

And you have to be disciplined here too, otherwise you are going to spend more money because of all the sales.

#24. Use Cash Back Apps

Another option in addition to coupons is to use apps like Ibotta and Shopkick.

These are by far my favorites.

Just download the free apps and get started.

With Ibotta, you earn cash back when you buy items at the store and scan your receipt. The also offer cash back for shopping online and for reaching milestones.

With Shopkick, there are numerous ways to earn kicks that you can redeem for cash or gift cards.

For example, you can earn kicks by:

- Walking into select stores

- Scanning product bar codes

- Linking your credit card

- Buying products

There are many more ways to earn with Shopkick and because of this, it is a must have app.

I’ve been using it for over a year now and have earned a handful of gift cards and cash.

To get started, just download the free app.

Android users click here and Apple users click here.

As a bonus, when you create your account, enter the code 250BONUS and you will earn an extra 250 kicks after your first store walk in or bar code scan.

#25. Make Your Home Energy Efficient

Another area that is a large expense for many households is electricity.

Luckily as with water consumption, there are some little things you can do to reduce your monthly bill.

- Install a programmable thermostat. A learning thermostat will greatly reduce your heating and cooling use and this will lower your bill the most. Here is the top rated one on Amazon.

- Caulk windows and doors. Feel around the trim of windows and doors in the winter and take note of any drafts you feel. Then get some caulk and seal the gap.

Just doing these 2 things will help to lower your electric bill. For more ideas to make your home energy-efficient, visit EnergyStar.gov.

#26. Use The Library

Do you buy a lot of books, music or movies? If so, you can save a lot of money by borrowing them from the library instead.

As long as you return the items by the due date, you won’t pay any late fees. And if you find something you love, you can still go out and buy it.

But you will save money on all the other things you would have bought and only watched, read, or listened to once.

Finally, many libraries now allow you to borrow a lot more than just the above mentioned items.

And many have partnered with Amazon so you can borrow books digitally and read on your tablet.

So take an hour and head to your local library to see what you can borrow.

#27. Wait 24 Hours Before Buying

I love this tip.

Since advertisers have gotten so good at tricking us to spend our money, we tend to impulse buy most of the time.

To beat them at their game, you need to have self-discipline.

How do you do this?

Before you buy anything, you have to wait 24 hours.

In most cases, you will forget about the item or the urge to buy it will subside. When this happens, congratulate yourself as you just saved yourself money!

And if you really want to take this tip to heart, take the money you would have spent, and transfer it to a savings account.

I did this for 3 months last year and my savings account grew by $435!

#28. Find The Right ATMs

Every time you use an out of network ATM or one other than your banks, you will be paying a service fee.

According to recent studies, the average ATM for out of network customers is close to $5!

If you use the ATM once a week, you are getting charged over $260 a year!

Take the time to figure out what ATMs you can use and not pay a fee.

Or see if there is an account at your bank that offers to refund you any ATM fees you pay.

Just note that many of these types of accounts require a higher average balance.

#29. Check Your Credit Scores

Do you know what your credit score is?

While a good score will help you to get a lower mortgage or auto loan rate, your credit score comes into play in other ways too.

For example, many insurers use your credit score to influence the premium you pay on your auto insurance.

Make sure you check your credit score once a year and work on increasing it if yours is lower than 650.

Luckily there are many things in your control that you can start doing to increase your score in a short amount of time.

Your next question is “where is the best place to get my credit score”?

I like Credit Sesame.

It is a free service that not only gives you your credit score, but it offers a ton of tips and tricks for how to increase your score.

#30. Review Your Credit Report

In addition to your credit score, you have to keep tabs on your credit report too.

Having misinformation here can cause you to have a lower than ideal credit score.

And by checking your credit report, you can be tipped off to any issues that might point to potential identity theft.

By staying on top of your credit report you can limit the damage and headaches of trying to get your identity back.

To get your credit report for free, your first and only stop should be with AnnualCreditReport.com.

There you can get a free score from each credit bureau every year.

#31. Ask For A Lower Interest Rate On Your Credit Card

Did you know you can save money by simply calling your credit card company?

If you are carrying a balance, a simple phone call can lower the interest rate you are paying.

Just ask if they can lower your interest rate. Most times they will start off by offering you a lower rate on new purchases.

This does you no good.

Politely decline and ask again. The lower rate they give you will be temporary, but it is better than nothing.

#32. Transfer Your Balance

Another great way to save money on interest payments and pay off your debt faster is by taking advantage of balance transfer offers.

With these, you usually get a 0% interest rate for 1 or 2 years. Of course, most will charge you a small fee for the privilege.

But even with the fee, you can come out ahead, as long as you pay off your balance during the promotional offer period.

Also, make sure you don’t start spending with your old card and carry a balance, otherwise transferring your balance is a waste of time.

#33. Consolidate Your Debt

If you have a lot of credit card debt, keeping up with the many monthly payments you need to make can become overwhelming.

The solution is to consolidate this debt into one debt.

Not only will you only have one monthly payment to make, freeing up time and lowering stress, but you should be able to get a lower interest rate too, saving you money.

My favorite service for consolidating credit card debt is Credible.

You enter in the details of the debt you want to consolidate and they will tell you what your new payment and interest rate will be, at no cost to you!

You choose to move forward or not.

#34. Prioritize Your Payments

If you use a strategy to pay off your debt, you can save money and get out of debt a lot sooner.

There are two popular methods for getting out of debt, the debt snowball and the debt avalanche.

With the debt snowball, you order your debts from smallest balance to biggest and make the minimum payment on all of your debts except the smallest balance.

For this one, you put as much money as you can towards it.

Once that debt is paid off, you take the next smallest balance and put as much money towards this debt while paying the minimum on all other debts.

The result of the debt snowball is paying off your debt quickly because you will be motivated and excited to do so.

With the debt avalanche method, you order your debts from highest interest rate to lowest.

Then you pay the minimum on all your debts except for the one with the highest interest rate.

Put as much money towards that debt until it is paid off, then move to the next highest interest rate debt.

The result of the debt avalanche is saving the most money on interest charges while getting out of debt.

Most people are better off choosing the debt snowball simply because of psychology. However, the debt avalanche will save you the most money on interest charges.

Be sure to think long and hard to determine which one is right for you.

Too many people get caught up in saving money on interest when the right choice for them is the debt snowball.

#35. Use Savings To Pay Off A Loan

If you’re close to paying off a loan and have the money in a savings account, consider using the cash to pay off the loan.

By doing this, you will save money on interest charges and free up money every month.

If you do decide to go this route, be sure to put extra money back into savings each month to build it back up quickly.

#36. Negotiate Debt With Your Creditors

If you have debt, see if your creditor will agree to a payment plan.

By choosing to go this route, you can save money on interest and your creditor might even be open to reducing your balance.

Before you jump on this tip, know that most times creditors will only negotiate with people who are having a tough time making payments in the first place.

#37. Use Spare Change to Pay Off Debt Faster

Getting out of debt should be your top priority because of the stress it adds to your life and because of the money you are paying in interest.

One of the simplest ways to help you pay off your debt quickly is to use Qoins.

Just link your credit or debit card and every time you make a purchase, Qoins will round up the amount to the next dollar and put that change in a savings account for you.

Then you tell Qoins what debt you want the money to go to and they will make the payment for you for a small fee.

Don’t think rounding up your purchases will make a difference?

The average user pays an extra $40 towards their debt every month.

That is an extra $480 a year!

#38. Review Your Rewards Credit Card

There are hundreds of credit cards out there and if you haven’t taken the time to do some review of the many options, you could be leaving money on the table.

For example, if you don’t travel frequently, is a credit card that offers miles per dollar spent your best option?

You might be better off with a cash back credit card instead.

To figure out what the best card is for you, take a few minutes to look at what you enjoy doing and where you spend the most money.

For me, a cash back card is the best option.

- Related: Click here to find the best cash back credit card

- Related: Click here to find the best travel rewards credit card

I take the cash back I earn and add it to my savings account.

And since I do the majority of spending at grocery stores and gas stations, the American Express Blue Cash card is the best fit for me.

By taking just a few minutes to pick the right card for you, you can make a serious impact on your finances.

I easily earn close to $1,000 a year in cash back that I invest.

In time, this free money is growing for me, making me wealthy.

#39. Scour Your Credit Card Statements

Do you review your credit card statements?

If you don’t you could be costing yourself a lot of money.

For example, by reviewing your monthly and annual statement, you can spot areas where you might be overspending.

Additionally, you might notice weird charges that you didn’t make.

By not reviewing your statement, you might pay for these fraudulent charges and pay more in the future.

When I was recently looking over my statement, I saw charges for ridesharing in another state. I hadn’t traveled recently, so the red flag was waving.

Sure enough when I looked into this, it was a fraudulent charge.

While the total amount wasn’t significant, I was glad I caught it early to prevent more headaches.

#40. Invest

To grow your wealth, you need to start investing.

Keeping your money in a savings account is great so you have some cash on hand, but not great for long-term savings.

Where do you go to get started investing?

Your best option is a robo-advisor as they handle the specifics when it comes to investing while you just set up a monthly amount to invest.

My favorite is Betterment.

They make investing easy and thanks to the tools they use, you can outperform the market over the long term.

In as little as 5 minutes you can have your account set up and let Betterment take it from there.

#41. Turn Your Hobby Into Cash

Do you make money on the side? If you don’t you are missing out.

There are endless ways for you to make up to $1,000 a month without much effort.

Making extra money on the side will completely change your life.

It will help you pay off debt, start saving for retirement, or even just ease your everyday spending by helping you to no longer live paycheck to paycheck.

Here is a great course that will help you to consistently make money month after month.

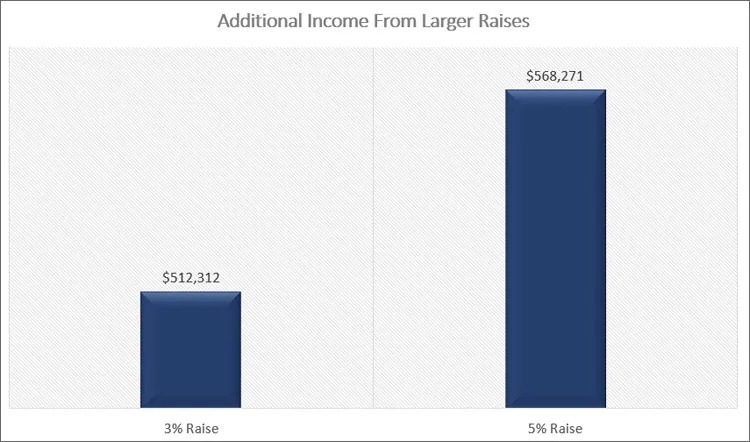

#42. Ask For A Raise

Your career is your greatest money making asset you have. If you are only earning 3% raises, you are missing out.

By taking some strategic steps, you can start to earn 5% raises every year.

How much of a difference does this make?

Let’s say you earn $40,000 a year now and earn a 3% raise for the next 10 years versus a 5% raise over the same period.

You end up making close to an additional $60,000 by getting larger raises.

Take the time to become valuable in your career and see your income grow.

#43. Refinance

Refinancing your mortgage is a great way to save thousands in interest and potentially lower your monthly payment at the same time.

For example, if you have a $200,000 fixed rate mortgage at 4.5%, you are paying $1,013 a month.

Over the entire 30 years, you will pay $164,813 in interest, assuming you don’t make any extra payments.

But if you refinance this loan into a new 20 year mortgage at 3.5%, you will pay $719 a month, saving you close to $300 a month or $3,500 a year.

And this doesn’t take into account the interest savings you will get as well.

You can play around with this calculator to see how much you could save.

And the savings don’t end with your mortgage.

You can refinance your student loans and save thousands as well.

My favorite service here is Credible.

You can get a free no-obligation quote on what your new interest rate would be along with your monthly payment.

If it looks good to you, you then decide to start the process.

I know a few friends who are saving over $10,000 by refinancing their student loans.

#44. Move

If refinancing doesn’t make sense for you, one option to consider is moving. Before doing so, look at how much your current house is costing you.

If it is eating up 25% or more of your income, you should look into moving.

By moving into a house or apartment that doesn’t cost as much, you will save money every month and every year going forward.

But don’t think you only can move across town.

If you live in a high cost of living area, consider moving somewhere else in the country.

When you move to a lower cost of living area, everything is cheaper. This includes housing, groceries, transportation, etc.

The trade off you face is potentially lower income from a job. Still it is worth looking into and running the numbers.

You may be surprised at just how much less it costs to live in some areas of the country.

#45. Review Your Insurance Policies

Having the right insurance is critical to your long term financial health. Remember the point of insurance is to protect you financially when things go wrong.

As a result, you need to make sure you have insurance for the right things and that you are paying a fair amount.

Sadly over time, the premiums you pay tend to rise. Most people accept this, but you don’t have to.

Be sure to shop around and compare quotes. By taking 15 minutes once a year, you ensure that you aren’t overpaying for coverage.

Don’t make the mistake many others do and assume you are paying a fair premium. Chances are you are not.

I found this out when I shopped around.

I was with my insurance company for over 5 years. I never thought to compare rates.

They treated me well and I accepted the rising premiums. But I decided to shop around, just to see.

I was blown away at what I found.

I ended up saving $300 that first year! I now shop coverage every other year.

Most of the time, I end up staying with my current insurer.

But there have been times I did switch and when I did, my average savings was $150 a year.

Take 15 minutes and make sure you are paying a competitive price on your insurance coverage.

You can start your comparison with Gabi Insurance.

Just link your current insurance account or upload your policy to Gabi and they will crunch the numbers to find you a better deal somewhere else.

It’s a quick and easy way to see where you stand and if you need to make a change.

Click here to get started.

Another insurer to look into is Liberty Mutual. They offer extremely competitive rates and partner with a lot of associations and colleges to offer huge discounts.

To see how much you can save, click here to get your free quote.

Next, if you have life insurance, it pays to get a second opinion here too. I love Bestow because of simple it is to get a free quote.

Finally, don’t overlook disability insurance.

Odds are you are more likely to get disabled than you are to die prematurely.

Breeze is a great place to get a no obligation disability insurance quote.

#46. Ask More Questions

When it comes to taking control of your finances, it is critical to always be learning more and educating yourself.

This includes asking lots of questions and reading lots of personal finance articles.

I’ve found that by reading others experiences and opinions, it opens my eyes for how I can be better with money.

Not all articles apply to me.

But many times I find they do and I can adjust what the author did for the idea to better fit with my life.

The result is a stronger financial foundation.

Related to this too is using tools to help you be a smarter consumer.

Using the best tools out there helps you to more easily control and handle your money.

And by using the right tools, it will give you more free time to spend doing the things you enjoy most.

#47. Set Calendar Reminders

Life is busy. This is especially true if you have a family.

Before I had kids, I thought time flew by. Now it seems like weeks go by in a blur.

Because of the hectic lives we live, it is easy to forget to pay bills from time to time or forget about upcoming events.

In fact, I missed my first credit card payment right after my daughter was born!

By setting up calendar reminders, you never forget about a payment or any to do item any more.

This helps to keep your finances and your life overall in the best shape possible.

#48. Change Your Passwords

How strong is your password? Do you use the same password for every account you have? Was the last time you reset your password never?

If you answered yes to any of these questions, it is time to update your password.

It is a simple task, but has a tremendous impact on your finances.

And it helps you to avoid headaches and stress should an account get compromised.

For example, a few years ago, my debit card was stolen. I don’t know how it happened, but I do remember looking at my bank account and seeing $300 missing.

At that time in my life, missing $300 was the difference of paying my bills this month and not.

Not only that, but I felt personally violated. I questioned how it happened and was fearful every time I handed my card to a cashier.

You don’t want to experience this. And you can avoid it by simply changing your password.

Here is a great guide on some ideas to make strong passwords you will remember.

#49. Consult A Professional

Does you financial situation overwhelm you? If so, it might make sense to talk to a professional.

While most financial advisors require you to have sizeable assets to invest, there are some out there that will look over your finances for you and make recommendations for a small one-time fee.

And it doesn’t stop with a financial advisor. You might be able to have your tax account review your finances as well.

#50. Skip The Trip

It is great to leave the stress from every day life behind and relax on vacation, but depending on your finances, you might have to skip a vacation this year.

But this doesn’t mean you can’t take some time off from work. If you have vacation days, be sure to use them.

You might have to enjoy a staycation instead of traveling somewhere.

While it doesn’t sound as exciting, you are making smart financial decisions that will benefit you in the years to come.

Wrapping Up

There you have 50 simple things you can do to give your finances a fresh start this year.

Don’t feel like you need to tackle every point on this list.

Start small and pick a few.

As you make changes and grow accustomed to the changes, you can start to take on new ideas from this list.

Over time, the benefits will be huge as you see a positive change on your finances and you life overall.